Not all “income” is taxed the same

When most people think of “income,” they think of a single number: their salary, or maybe their business profit. But for tax purposes, Canada treats different kinds of income very differently.

Broadly, you can think about four main buckets:

1. General (ordinary) income – taxed the heaviest

This includes:

- Employment income (T4 salary, wages, bonuses)

- Self-employment income and professional income

- Sales commissions, tips, gratuities

- Most pensions and many government benefits

- Interest income from GICs, savings accounts, and bonds

This category is taxed at your full marginal tax rate. For many Canadians in mid-to-high brackets, that can easily mean 30–50%+ combined federal and provincial tax on each extra dollar.

If all or most of your income lives in this bucket, your ability to build wealth is fighting a constant headwind.

2. Dividend income – preferred tax treatment (if planned properly)

Dividend income comes from owning shares in corporations:

- Public company shares (through a brokerage)

- Private corporation shares (e.g., your own company)

Eligible and non-eligible dividends receive preferential tax treatment through the gross-up and dividend tax credit system. In plain language, dividends are taxed more gently than salary or interest at many income levels, especially in non-registered accounts.

But this is not one-size-fits-all:

- The benefit varies by income level and province.

- How you mix salary and dividends from a corporation affects both your personal and corporate tax picture.

Used strategically, dividends can help you lower your overall tax burden and control your cash flow more precisely year to year.

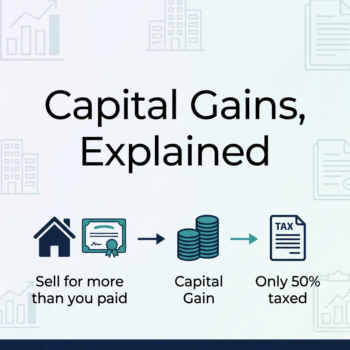

3. Capital gains – only a portion is taxed

A capital gain is the profit you make when you sell a capital asset for more than its adjusted cost:

- Stocks, ETFs, mutual funds in a non-registered account

- Rental properties, cottages, and other real estate

- Shares in a private corporation

- Certain business assets

In Canada, only a portion of the capital gain is included in your taxable income (the “inclusion rate”), and that portion is then taxed at your marginal rate. This makes capital gains one of the most tax-efficient forms of income compared to salary or interest.

Your principal residence is generally exempt from capital gains tax when it qualifies, which makes it a unique and powerful planning tool when used wisely.

Because you can often choose when to sell, capital gains also give you flexibility to:

- Spread gains over multiple years

- Offset them with capital losses

- Time big sales around lower-income years

All of this can dramatically reduce lifetime tax if you plan ahead.

4. Tax-free income – the most powerful (and most overlooked)

Yes, some income can be truly tax-free. Examples include:

- Gains and withdrawals from a Tax-Free Savings Account (TFSA)

- Proceeds from the sale of your principal residence (when conditions are met)

- Certain insurance benefits and policy loans

- Some gifts, inheritances, and lottery winnings

On top of that, loan proceeds themselves are not income—so leveraging home equity or properly structured insurance can create cash flow without triggering immediate tax.

This fourth bucket is where you can create genuine acceleration in your wealth plan: money that grows and comes out to you with no additional tax bill.

Why this mix matters more after tax season

We’ve just come through another personal tax filing season. For most people, that means:

- Downloading tax slips and organizing many tax documents

- Filing your tax returns yourself or using the services of an accountant

- Getting a refund or paying a balance owing

- Moving on and forgetting about tax for another year

But if you only think about tax once a year at filing time, you’re missing the real opportunity.

The real power is in planning which types of income you’ll earn, and when you’ll earn them, long before next April:

- Shifting from fully taxed general income to more dividends and capital gains where appropriate

- Using TFSAs and other tools to build up truly tax-free streams over time

- Structuring corporate income and withdrawals in a tax-smart way if you’re a business owner

The difference between someone who does this intentionally and someone who doesn’t is often hundreds of thousands of dollars over a working lifetime.

A simple reflection to start today

Ask yourself:

- What percentage of my income is currently in the fully taxed bucket (salary, interest)?

- How much am I deliberately building in the capital gains and tax-free buckets?

- If I keep doing exactly what I’m doing now for the next 10–20 years, am I happy with where I’ll end up after tax?

If you don’t like the honest answer, that’s not a failure—it’s a starting point.

Your next step: join us at the Tax-Efficient Wealth Summit

This June, I’m hosting the Tax-Efficient Wealth Summit, where we go much deeper into:

- How these four income buckets really work in Canada

- How to design your personal “income mix” so more of what you earn actually stays with you

- Practical tax planning strategies for employees, professionals, and business owners

- How to align your tax strategy with a long-term wealth plan, not just a one-year refund

If you’re serious about turning this past tax season into a wake-up call—not just a yearly chore—this is where we start turning knowledge into action.

Reserve your spot for the Tax-Efficient Wealth Summit here:

https://taxefficientwealth.ca/summit/