Why inflation will ruin you financially if you don’t protect your wealth

“Inflation is taxation without legislation.” — Milton Friedman

There is some element of truth to Friedman’s definition of inflation, but what really is inflation?

Inflation is the rate at which the general level of prices for goods and services is rising.

In my book, I refer to inflation as the silent killer as we rarely see it. While most people are familiar with inflation, we often underestimate the powerful impact it has on our ability to grow our wealth and eventually achieve financial freedom.

Ironically, we often think of financial freedom in terms of dollar value rather than in terms of the purchasing power of our dollars (the amount of goods and services you can buy). If you’re unable to acquire what you need when you need it, then you’re not necessarily financially free.

“Invest in inflation. It’s the only thing going up.” — Will Rogers

So, what’s the big deal about inflation, and why should we care?

If you had a $100,000 income 5 years ago, you could probably afford a decent starter home, take care of your expenses, and have little left to save and invest.

Today, if you earn $100,000 income, your purchasing power will be less than it was a few years ago. You likely cannot afford a house today (particularly in the metropolitan cities) and even if you can afford one, you will end up incurring debt to keep up with your expenses.

In simple terms, a $100,000 income a year ago with a 5% annual inflation is only worth $95,000 today. And if you consider the fact that the tax rate will increase with time, you can now see why inflation will quickly become a significant obstacle to building sustainable wealth.

“The natural tendency of the state is inflation.” — Murray Rothbard

For those that understand the world economy at a deeper level, you know that inflation will never go away. In fact, the Canadian government and other governments around the world intentionally create inflation with policies. They need inflation to deal with the rising debt crisis.

To provide a bit of insight, the global debt of the world adds up to $255 trillion. This amount is over three times world GDP, this ratio is even worse if you look at countries like the United States, Japan, and some European countries. This debt level will exponentially escalate as governments around the world are dealing with the ongoing health, war and economic crisis.

When our (any) government increases the supply of money, the purchasing power (value) of every dollar declines.

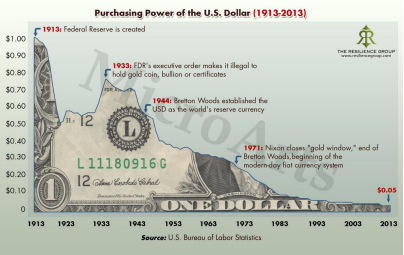

The chart below from The Resilience Group shows the massive decline in the purchasing power of one dollar from 1913. In the 100 years that were tracked, the purchasing power of a dollar decreased by 95 cents.

In his book, “The Bitcoin Standard,” Saifedean Ammous writes that the supply of money is controlled by the central bank, and they can increase the supply of money by:

- “Reducing interest rates, which stimulates lending and increases money creation.

- Lowering the required reserve ratio, allowing banks to increase their lending, increasing money creation.

- Purchasing treasuries or financial assets, which also leads to money creation.

- Relaxing lending eligibility criteria, allowing banks to increase lending and thus money creation.”

All of which they’ve done on massive levels. This is how they got us out of the 2008 market crash and the 2020/2021 Covid-19 pandemic.

As Judd Gregg writes in a recent article, When the dollar is worth 60 cents,

“In just the last two months of this federal fiscal year (2020), the deficit run up by the U.S. government has exceeded $1.3 trillion.”

He goes on to write,

“To give some context to the gigantic size of this spending, these two months of deficits exceed by a factor of three the largest annual deficit generated during the term of President George W. Bush, and blow past the largest annual deficit run up by President Obama.”

Even without further spending, Judd writes that the U.S. government is headed toward almost $4 trillion in deficit spending, accompanied by somewhere near $10 trillion of financial infusion by the Federal Reserve.

An important question to consider is: who will pay all of this debt? The reality is that these debts will never be repaid as they’ve grown to levels that is now unmanageable. As a result, currencies will continue to devalue, allowing this debt to be wiped away via inflation.

Eventually, with this trend, we will get to a point where countries will be forced to go bankrupt and our dollar will devalue to a point where we only get back pennies on the dollar.

“Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.” — Milton Friedman

To the regular taxpayers, this may seem unlikely but to the tax-smart individuals, they expect this and this will inform decisions on planning strategies to invest wisely and to protect wealth.

So, what can you do to protect yourself? What can you do to fight this imminent inflation?

Here are a few suggestions:

- Invest in real estate — it is a great hedge for inflation.

- Invest in precious metals like gold and silver — history suggests that these metals hold their values when everything else crumbles.

- Invest in yourself — arm yourself with knowledge that no one can take away.

- Invest in your precious relationships — at the end of the day, we are social animals that rely on one another. To minimize anxiety, depression, and other mental problems, lean in on your relationships.

- Invest in your spirituality — whatever this looks like for you, know that we live and exist for something bigger than ourselves.

“Inflation is like sin; every government denounces it and every government practices it.” — Frederick Leith-Ross

P.S. I am on a mission to arm you with financial education. That’s one reason I wrote Tax-Efficient Wealth and this is why I’m also hosting the Tax-Efficient Wealth Summit again this year. To learn more about the summit and to join us, go here.

{kind=link}